$50,000 a Year is How Much an Hour?

If you decided to stop working at your current job, would you be willing to start a new job that pays $50,000 a year? Some might say yes, others say no, and others say they don’t know. But despite all these answers, it boils down to knowing exactly how much $50,000 is a year. Is it a lot of money, or is it just a small amount of money? If you were looking for a job in some states like Colorado and New York, you would have to include a salary range in your job posting which is why you have to know this, so you don’t sell yourself short.

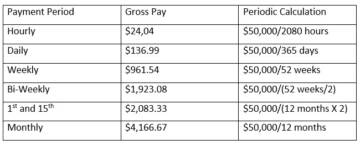

$50,000 a Year is How Much an Hour?

To fully understand how much money $50,000 a year is, you have to know how much it is per hour. To know this, we have to do some mathematics. If someone works at a job for 40 hours weekly, they will be working for 2,080 hours a year, assuming that they had not taken a day off and it’s a full-time job. If they were making $50,000 a year, that would be $24.04 an hour. This seems like a decent income at first, but it might not be as attractive as it sounds when you start to factor in your bills and taxes. Instead of working 40 hours a week, you worked 50 hours a week, which is usually the standard for a salary earner. This would mean you would be earning $961.54 weekly and $19.23 an hour. This would also exclude benefits and days off.

If you don’t get a clear picture of how it works, the table below may help. It helps ease the stress of using a calculator.

Is $50,000 a Year Enough After Taxes?

You should know that just because you make $50,000 a year doesn’t mean you’ll take that amount home annually; you still have to pay your taxes, which will affect how much you take home annually. Figuring out how much you get to pay in tax is an essential aspect of understanding your pay, as it allows you to know how much you’ll be making at the end of the year. So let’s do that calculation.

Assuming you’re a single filer and you reside in the state of California, which has a high-income tax rate, you would have to pay $9,675 in federal and state taxes, which is a rough estimate, and your final take home would be $40,325.

If you reside in Florida, which has no state income tax, you would be paying $8,140 in federal taxes, and your take home would be $41,861.

So the amount you pay in tax is dependent on your state of residence. It is safe to say that these are just rough estimates of what you’ll pay in taxes, but if you want to be safe, take out 30% of your income as a tax budget. Consider moving to a state that doesn’t tax your wages, like Alaska, Florida, Tennessee, or Texas.

Factors That Affect Your Take Home

Aside from taxes, there are many other things that could affect the amount of money you take gross pay or take home. While taxes usually take a large chunk, things like insurance could also affect your gross pay. (This does not include benefits.) Some of these include:

Paid Off Time (PTO)

One of these things includes PTO. Paid-off time usually varies between jobs and employers, and your gross pay could be affected by the PTO you’re given. If you are given three weeks of paid time, you would only have to work for 1,960 hours a year. This would be less than the usual 2,080 hours, which would drive your hourly rate to about $25.51. This would affect your gross pay.

Insurance Plan

Your insurance plan also matters. If you get your insurance through your employer, your hourly rate could increase. You could also get an increase in your hourly rate if you get tuition assistance. These are benefits that could help, and these should be included only if you plan to use them. If you won’t be using them, they are not beneficial.

What About Retirement?

This is also something that you could factor into your annual salary. If you put your money into a retirement plan sponsored by your employer, then that would be a smart move for your financial life in the long term. It is something you should do. Most employers usually match a certain percentage of the pay you put in a retirement plan, so if you were to put in 5% of your gross income, they would match 5% of it. This is a general figure that most companies would contribute so that it would be safe. It is also safe to note that this is why this would affect your annual take home; it was safe financially.

So if you were making $50,000 a year and getting a monthly payment, then your gross pay would be about $4,100.67 monthly, and then you contribute 5% to a retirement plan, this would be $208.33, and after taxes, your take home would be about $3,958.34. Annual, you would have $2,500 less, but it would be worth it, as you would be saving for your future.

$50,000 might be a lot of money for you, but before you decide, you should remember to take out your taxes, bills, and other expenses. Then you can determine whether the money is worth the job. It depends on what you think you can handle.

Jason Butler is the founder of My Money Chronicles and an SEO consultant with over a decade of blogging experience. Since 2015, he has earned income through side hustles including blogging, eBay flipping, affiliate marketing, and freelance work while paying off over $64,000 in debt. His work has been featured in Forbes, Discover, Investopedia, and Yahoo Finance.